März 04, 2026

Supply Chains

Industry Analysis

When the Iran Conflict hits the Medtech Supply Chain

When tanker traffic slows in the Strait of Hormuz, most observers first think about oil prices. Yet the consequences extend well beyond energy markets. The medical technology industry—with its highly globalized supply chains—can also feel the effects of geopolitical shocks surprisingly quickly.

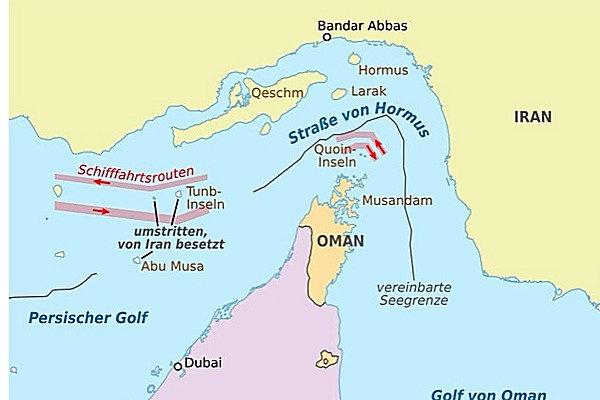

Map of the Strait of Hormuz between Iran and Oman, one of the world’s most important maritime chokepoints for global energy and trade flows.

Map: NordNordWest / Wikimedia Commons (CC BY-SA 3.0)

Many critical components used in medical devices depend indirectly on the very factors that conflicts in the Gulf region tend to disrupt: transportation, energy prices, and industrial raw materials.

For medtech suppliers and device manufacturers, the current conflict could therefore translate into new cost pressures and supply chain risks.

Why Global Supply Chains Make the Industry Vulnerable

Although medical devices themselves are rarely manufactured in the Middle East, the industry relies heavily on international supply networks.

The conflict primarily affects the sector through three indirect channels.

1. Logistics

Rising insurance premiums and potential shipping reroutes increase transportation costs and may extend delivery times—particularly for air cargo and spare parts.

2. Energy

Higher oil and gas prices increase the cost of energy‑intensive manufacturing processes.

3. Raw materials

Industrial metals and petrochemical inputs may become more expensive, directly affecting component costs.

For an industry built on globally distributed supply chains, these factors can quickly become relevant.

Example 1: Imaging Systems and Complex Supply Chains

A typical MRI or CT system consists of thousands of components sourced from multiple regions:

• electronics from East Asia

• precision mechanics from Europe

• sensors and control electronics from the United States or Japan.

Manufacturers of imaging systems such as Siemens Healthineers therefore operate highly complex global supply chains.

If shipping times increase or electronic components arrive late, installation of imaging systems at hospitals can easily be delayed by several weeks.

For OEM manufacturers, this can result in:

• postponed project revenue

• higher logistics costs

• increased inventory requirements for critical spare parts.

Example 2: Consumables and Petrochemical Dependence

Another segment that reacts particularly sensitively to energy prices is single‑use products and consumables.

Many products—including catheters, infusion sets, and diagnostic disposables—are based on petrochemical plastics.

Manufacturers such as B. Braun operate large production facilities for these products, often involving energy‑intensive processes such as injection molding, cleanroom manufacturing, and sterilization.

Rising energy prices or higher polymer costs can therefore translate directly into higher production costs.

For consumables with relatively tight margins, this effect can be particularly significant.

Why Europe Could Be More Exposed

The impact of the conflict may vary by region.

Europe—and Germany in particular—is generally more sensitive to energy price fluctuations than the United States.

Many European medtech suppliers manufacture plastic components, sterile disposables, and precision parts using energy‑intensive processes.

Higher gas or electricity prices may therefore quickly translate into higher manufacturing costs.

In the United States, companies may focus more strongly on risks related to global component sourcing, export controls and sanctions, and hospital capital expenditure budgets.

Five Takeaways for Medtech Suppliers

1. Logistics is becoming a risk factor again

Higher transport costs and longer delivery times may delay installations and service operations.

2. Energy prices affect consumables first

Plastic‑based products are particularly sensitive to energy and raw material costs.

3. Raw material volatility could increase

Industrial polymers and metals may experience stronger price fluctuations.

4. OEMs are reassessing their supply chains

Dual sourcing and regional supplier networks are gaining importance.

5. Supply chain resilience is becoming a competitive advantage

Suppliers able to guarantee stable delivery may become strategically more important to OEMs.

Conclusion

For many companies, the current crisis is another reminder of how dependent the medtech industry has become on global supply networks. Following the pandemic, semiconductor shortages, and rising geopolitical tensions, supply chain resilience has once again moved to the top of the agenda. Many OEMs and suppliers are already investing more heavily in dual sourcing, regional manufacturing, and larger safety inventories.

The key lesson for the industry: In a globalized medtech sector, geopolitics no longer stops at the factory gate—it has already made its way onto the bill of materials.

Author: Sandra Heeg

© 2026 Sandra Heeg. All rights reserved. Copyright retained by the author. Publication on medtechmediaeurope.com is permitted by the author and may be withdrawn at any time.